September industrial production: A mild recovery amidst general pessimism

sanayi-uretim

sanayi-uretim

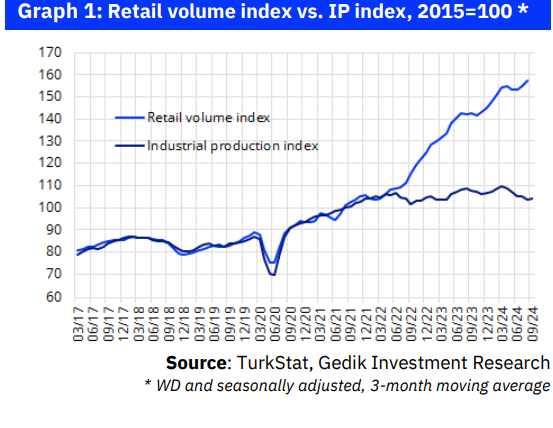

Tukey’s IP rose on a MoM basis but remains at depressed levels not observed since the heydays of the Covid-19 pandemic Judging by October ISO-S&P Global manufacturing PMI, the lackluster trend in production is set to continue. On the other hand, retails sales are staging a more durable recovery, while Turkstat and BloombergHT consumer confidence indices rebounded sharply since summer months. The gap between retail sales and production is inflationary and in contradiction with CBRT assertion that Turkey’s output gap is widening.

After reviewing the data, chief economist of HSBC Asset Management Mr İbrahim Aksoy forecasted 3.5% GDP growth for 2024.

Our regular contributor Mr Serkan Gonencler reviewed the data for PATurkey:

The industrial production (IP) index rebounded by 1.6% MoM, but contracted by 2.4% in YoY terms. TurkStat announced that the seasonally and WD-adjusted IP index showed a monthly increase of 1.6% in September.

Despite this increase, the index remains 5.7% below its peak in February of this year. On a YoY basis, the WD-adjusted index indicated a 2.4% YoY decline, while the unadjusted index showed a 4.4% drop, marking the fourth consecutive month of year-over-year contraction (-5.0%, -3.9%, -5.2%, and -2.4%).

Quarterly data shows that the IP index contracted by 3.8% YoY in 3Q24 following the 1.9% shrinkage in 2Q24.

For the January-September period, there is a limited YoY decline of 0.3%. Examining the longer-term trend, we see that the IP index continues to remain below levels reached at the end of 2021.

While certain sectors have outperformed, there is still a general weakness across the board. For the January-September period, despite the overall subdued performance in most sectors, some key sectors like food, chemicals, basic metals, and electrical equipment have shown resilience. During this period, in YoY terms, the food sector recorded a 3.6% increase, chemicals rose by 3.5%, basic metals by 5.9%, and electrical equipment by 3.8%.

On the other hand, sectors that registered annual contractions include apparel (-8.4%), textiles (-7.2%), plastics and rubber (-4.7%), motor vehicles (-3.6%), textiles (-2.3%), non-metallic mineral products (cement, glass, ceramics) (-2.0%), and metal products (-1.8%).

Some sectors with relatively lower weight in the index displayed double-digit or near-double-digit declines in production: leather (-14.0%), tobacco (-9.4%), computers (-8.8%), wood products (-8.5%), and pharmaceuticals (-6.4%).

The manufacturing PMI suggests that the annual contraction in the IP index may continue in the coming months.

Although the PMI rose from 44.3 in September to 45.8 in October, it remained below the 50.0 threshold for the seventh consecutive month. In fact, excluding the levels of 50.2 and 50.0 in February and March this year, the manufacturing PMI has been below the 50 threshold since July 2023, with an average PMI reading of 48.3 during this period. The current PMI levels indicate that we may continue to see YoY contraction figures of close to 4.0% in the IP index over the next few months.

While the industrial production remains weak, there are signs of a resurgence in consumption trends.

Despite this production weakness, we observe that consumer spending, which had shown only limited cooling, has started to pick up again in recent months. For instance, the sequential growth in the retail sales volume index returned to positive territory over the last three months (June-August), while there was a 13.3% YoY increase in August. We have also been witnessing some improvement in confidence indices, which may be reflected into consumption trends. We will have a clearer view of consumption trends, when the TurkStat releases September data for the retail sales volume index alongside domestic trade volume and service turnover indices.

That said, we have already observed an increasing trend in the YoY increase of credit card spending in September and October, which is closely correlated with the retail sales volume index. This indicates that we may also see strong retail sales figures tomorrow. This could be seen as contradicting the CBRT’s view that domestic demand has declined to levels supportive of the disinflation process.

By Serkan Gonencler, Chief Economist, Gedik Invest

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/