In 2Q24, the QoQ GDP growth rate slowed to 0.1%, while the YoY growth rate was 2.5%.

TurkStat announced that the annual GDP growth for the second quarter was 2.5%, which slightly fell short of our and the median market expectation of 2.8%. Although the seasonally and WD-adjusted quarterly GDP growth rate seems to have declined from 1.4% in the previous quarter to 0.1%, it actually points to a stronger growth performance than our expectation of a 0.7% quarterly contraction.

Significant revisions in GDP growth figures for previous quarters have led to deviations in forecasts.

We observe that there have been significant revisions to the growth figures for previous quarters; figures for 2023 have been revised upward, while the 1Q24 GDP growth has been revised downward. For instance, the YoY GDP growth for 2Q23 was revised from 3.9% to 4.6%, and the overall GDP growth for 2023 was revised from 4.5% to 5.1%, while the 1Q24 GDP growth was revised from 5.7% to 5.3%. When looking at quarterly growth, the 2.4% growth for 1Q24 was revised to 1.4%. We think that these revisions have had a significant impact on the deviations in growth forecasts.

Considering these revisions, we can say that the second quarter actually demonstrated a better growth performance than expected. Even though all indicators, such as industrial production index, the services production index, and the retail volume index, point to a contraction compared to the previous quarter, the headline GDP continuing to grow by 0.1% confirms this expectation.

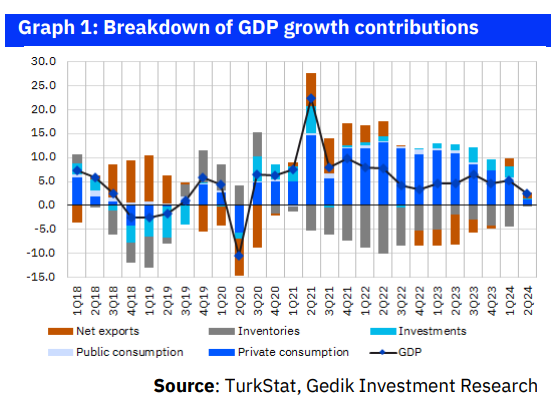

There was a noticeable slowdown in domestic demand in 2Q24.

Private consumption expenditures, which have been the main driver of growth since 2021, showed a noticeable slowdown in the second quarter. The annual growth rate of private consumption expenditures, which recorded an annual growth of 13.6% for the whole of 2023, appears to have slowed to 6.8% in the first quarter and 1.6% in the second quarter. As for investment expenditures, another significant component of domestic demand, there was only a 0.5% YoY growth.

Considering the 0.7% YoY increase in the government’s final consumption expenditures, the contribution of domestic demand to headline growth emerges as only 1.4%. Despite the slowdown in exports, the more pronounced slowdown in imports results in a positive contribution of 1.3% from net external demand (similar to the previous quarter). The negative impact of inventory accumulation has also receded to -0.2%. From the production perspective, the divergence between the industrial and services sectors has become more pronounced, with the industrial sector contracting by 1.8% year-on-year. However, a significant slowdown trend has also emerged in the services sectors.

GDP growth for 2024 could fall below 3.0%.

In summary, the breakdown of second-quarter GDP growth indicates a more pronounced slowdown in domestic demand, while leading indicators suggest that this slowdown may persist in the period ahead. Considering the upward revision of 2023 GDP growth from 4.5% to 5.1%, we believe that that downside risks are now more pronounced for the 3.0% GDP growth forecast for 2024. Despite the slowdown in domestic demand, it should be noted that this is not yet a slowdown of sufficient magnitude to support a sustained disinflation process.

Chief Economist Serkan Gonencler, Gedik Invest Research

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/