PA Turkey’s coverage of Turkey’s 2025 outlook starts with the view from OECD, published in its December report. The report states that growth will moderate, which will lower inflation somewhat, as the external deficit remains manageable for a second year in a row. A face-about from current tight fiscal and monetary policies remains a serious risk, while structural reforms are need to achieve sustainable progress against inflation.

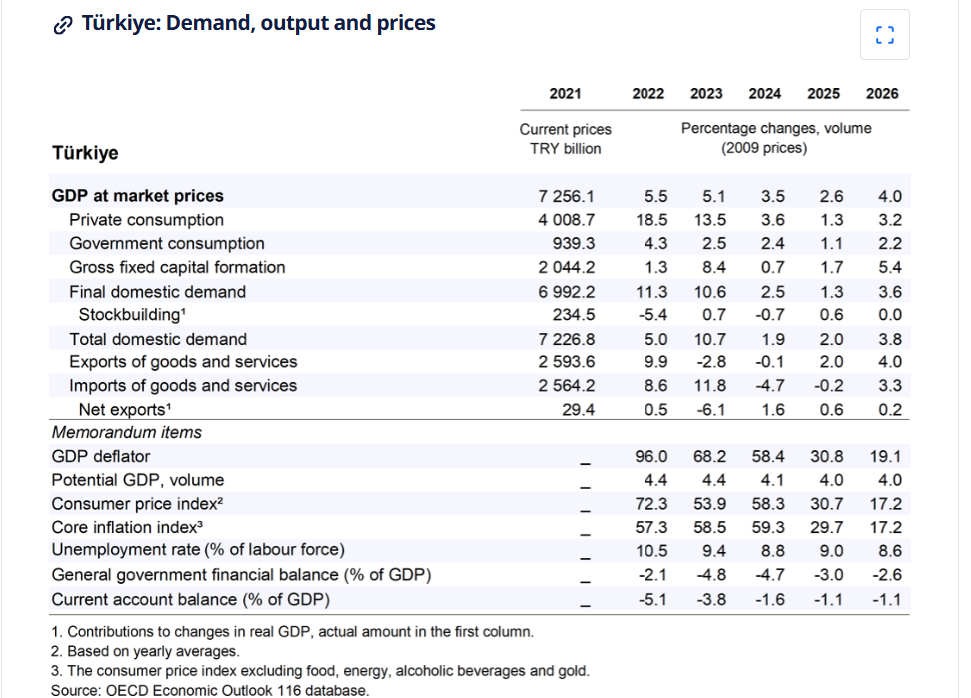

Economic growth will ease to 3.5% in 2024 and 2.6% in 2025 as necessary macroeconomic stabilisation policies will slow domestic demand. Tighter financial conditions and ongoing fiscal consolidation will limit household consumption. Investment and government consumption will also slow as the effects of the post-earthquake reconstruction wear off. However, exports should increase on the back of an improvement in the external environment and a continued revival of international tourism. GDP growth is projected to rebound in 2026, reaching 4% as the effects of the stabilisation policies ease.

The fiscal and monetary policy mix is rightly tight and should remain so until inflation is firmly on a path to target. Despite the ongoing price moderation, high inflation expectations and strong inertia uphold upside risks on the inflation outlook. Structural reforms can further support the current efforts to stabilise the macroeconomic framework and raise the long-term growth potential. In particular, labour market reform would help increase high-quality formal job creation.

Growth has slowed considerably

The economy has slowed in 2024, with year-on-year GDP growth dropping from 5.3% in the first quarter to 2.5% in the second quarter. Tight financial conditions weigh on domestic demand, causing household spending and investment to slow significantly. Leading indicators like manufacturing capacity utilisation, the purchasing managers index, services production, along with an ongoing contraction in commercial loans in real terms, indicate that economic activity could slow further. Both the employment rate and labour force participation remained stable in the first half of 2024. In September, annual consumer inflation fell below 50%, largely due to base effects. However, core inflation remained high, driven by inflation in services and rising goods inflation. Inflation expectations are declining but are still elevated.

CURRENT ACCOUNT

The current account balance has improved due to the rebalancing of the drivers of economic growth, positive outlook in tourism and natural gas production in the Sakarya field. Foreign exchange reserves have been increasing. Although, exports have been sluggish in recent months due to seasonal factors and escalating regional tensions, they are expected to contribute to further improvements in the current account balance, in line with the government’s efforts to shift economic growth towards exports.

Monetary and fiscal policy will remain tight

The monetary and fiscal authorities have both reiterated their commitment to keep policies tight as part of the multipronged effort to put Türkiye’s economy back on a sustainable path. The central bank has recently kept the policy rate at 50% but indicated that it will decisively use all the tools at its disposal in line with its main objective of price stability. It also tightened macroprudential policies by introducing a 2% monthly growth limit for foreign currency loans, that has subsequently been lowered to 1.5%. The government published its Medium Term Programme, confirming the commitment to reduce the public sector general deficit from 5.6% in 2023 to 2.6% in 2026. This effort is partly based on tax revenue increases, including a new minimum corporate tax and the removal of exemptions. Larger deficit cuts will come from the expenditure side through reduced capital and transfer spending as earthquake-related investments will largely decrease in 2025.

The economy will moderate

Economic growth is expected to slow after years of robust but unsustainable growth driven by domestic demand. Tighter financial conditions coupled with restrictive monetary and fiscal policy will hamper household consumption, especially as the effects of post-earthquake reconstruction fade. Unemployment will rise slightly but stay around 9%. The measures to contain inflation will have an impact, but nevertheless inflation will decline only gradually, staying above the 5% target through the forecast period. The main risk to the outlook stems from the potential relaxation of the current macroeconomic stabilisation policies, which could lead to higher inflation and further instability. In contrast, further credible policy improvements in fiscal, financial, and monetary policy might improve investors’ sentiment and strengthen growth.

Monetary and fiscal policy should remain on course

Despite its negative impact on domestic demand, the new restrictive setting of monetary and fiscal policies has helped to stabilise the financial market, boosted confidence, and reduced uncertainty. To fully leverage the improving international sentiment, authorities should maintain macroeconomic stabilisation policies until inflation is firmly on track to meet targets. Alongside current consolidation efforts, the government should continue to closely monitor risks from contingent liabilities. A stable and predictable policy framework, along with a stable macroeconomic environment, could significantly attract international investment. Structural reforms can further support these stabilisation efforts and enhance long-term growth. For instance, labour market reforms could promote higher-quality formal job creation by making permanent contracts more flexible and ensuring that minimum wages are affordable for businesses. Improving the skills of both current and new employees can help reduce the negative effects of the skilled labour shortages impacting Turkish companies.

Follow our English language YouTube videos @ REAL TURKEY: https://www.youtube.com/channel/UCKpFJB4GFiNkhmpVZQ_d9Rg

And content at Twitter: @AtillaEng

Facebook: Real Turkey Channel: https://www.facebook.com/realturkeychannel/