Turkish Equities Quarterly Strategy Report: Adjusting to the Post Pandemic Environment

piyasalar

piyasalar

The World: The ongoing energy crunch causing various knock-on effects is triggering fears of stagflation.

- The recovery in the Global economy remains on track, despite some loss of momentum recently. The slowdown seems more pronounced for the U.S. and China in particular, while the Eurozone growth is relatively stronger. As such, growth estimates are being downgraded for the U.S. and China and upgraded for the Eurozone.

- Despite signs of peaking in US inflation, whether the high inflation will be transitory or remain to be a hot debate amidst the ongoing disruptions in supply chains and supply side shortages, and recently, the spiking energy prices. Although FED maintains its expectation that the spike in inflation will be transitory, it also admitted that inflation may remain at current high levels for longer than initially expected. The FOMC brought forward further the projected initiation of the rate hike process, and revealed that might initiate the tapering process soon, as well as clarifying that they are planning to end the tapering process by the end of 1H22. US- yields also reverted back to above 1.50%, which has been another factor trimming the risk appetite.

- The energy demand-supply mismatch at the post-Covid recovery depleted stockpiles as a result of extreme weather conditions, and but probably most importantly, the World’s efforts to cut down its dependency on fossil fuels and shift to renewable energy sources. These have caused a mounting of energy prices ranging from oil and natural gas to coal. Rising energy prices have also been causing various knock-on effects from economic growth prospects to significant inflationary impacts.

- The massive debt load of the Evergrande, China’s real estate giant, has been leading to fears of contagion and systemic risk in the Chinese economy. The authorities’ efforts to cut down the economy’s dependency to credit-oriented growth and energy prices have also been increasing the risks of a sharper than desired slowdown in economic growth.

- Amidst these issues, fears of stagflation in the World economy in 2022 seems to have risen considerably recently, although not yet priced in. Although the global risk appetite has been curtailed noticeably, the retreat in Global equities, in the U.S. in particular has been rather limited. As such, also considering that the U.S. markets are very close to historical highs, the probability of a major correction remains alive.

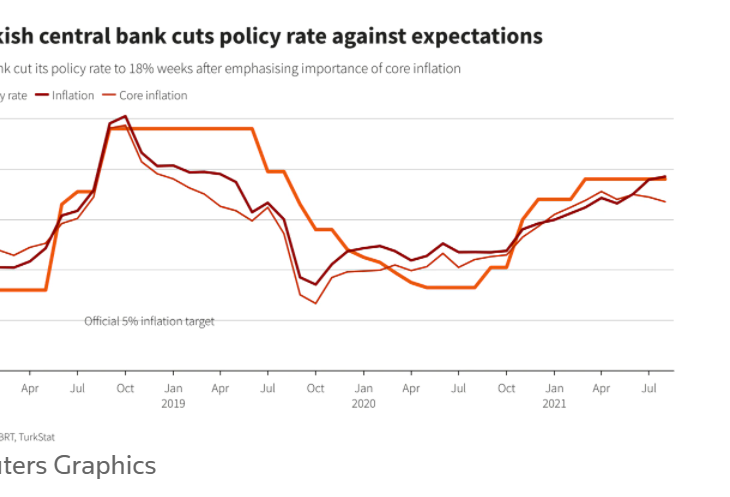

- CBRT already signalled that it is inclined to keep on with the rate cut process going forward by shifting its focus to core inflation, and by actually initiating the monetary loosening process earlier than expected in September, with an unexpected 100-bps cut, as well as by removing the «tight monetary policy stance» phrase from the MPC statement. Yet, September core inflation components were rather high, and this together with the ongoing weakening trend in TL actually makes it difficult for the CBRT to keep on with the rate cut process.

- CPI inflation may actually test 20% levels in October, particularly due to the ongoing hikes in food prices to be followed by some deceleration over the last two months of the year with the help of base effects. We would still expect year-end CPI inflation at close to 19.0%, which is in fact considerably higher than recent market expectations. Yet, following this period, we expect CPI inflation to exceed 20% in early 2022, attributable to a spike in energy inflation and potential FX pass-through particularly in core inflation components due to the weakening in the TL.

- We still are not ruling out the possibility of the continuation of the rate cut process (if not in October) despite the gloomy inflation Outlook. This could risk the need of these cuts to be reversed in the foreseeable future.

- Even though we would expect some slowdown going forward, the ongoing export performance and the y-t-d growth performance suggests that 2021 GDP growth will end up at about 8.5%, or probably above. That said, we also expect YoY IP growth rates to significantly lose momentum starting from early 2022, (to probably close to zero) as strong base effects kick in.

- The budget deficit remains below 2.0% of GDP as of September. Considering the current growth pace, we believe that the budget deficit/GDP ratio may end up slightly below the 3.5% target in 2021.

- C/A deficit has declined to USD23bn by August from close to USD37bn in early 2021 and should decelerate further to USD19bn in September. From that time on, we expect a flattish trend in C/A deficit until year-end despite robust export prospects, due to the rising energy import costs, and maintain our end-2021 C/A deficit expectation at close to USD19bn.

In our view, the key challenge of Turkish stocks is not understanding corporate business models and valuations, but rather to gauge the timing of a sustainable drop in risk premium/interest rates - Turkish stocks remain cheap and offer superb opportunities for long term investors, but short/medium term challenges could maintain pressuring prices.

- The BIST remains as a substantial underperformer against the GEM’s with an all time low relative performance level.

- The index returned 26% in 2020, so far declined by 4% in 2021. Its relative performance was -18% in 2021 and -16% so far this year. Turkish stocks trade at a 28% EV/EBITDA discount compared to their EM peers, slightly less than the 33% at the end of 2020. On the other hand, given our macro discussions mentioned so far in this report, it is clear that the probability for a catalyst to close this discount remains low for the next 3-6 months. Banking stocks, the private names in particular, should report better results in the second half of the year, led by margins and lower cost of risk. Yet, unstable currency and lack of visibility in monetary policy are unlikely to make up for the gap on concerns over longer term earnings, for now.

- Maintaining our fair value estimate for the BIST-100 at 1,680 level. This level is likely to be reviewed following of the announcement of third quarter results, which starts this week. Please note, we currently use 16% as our DCF risk free rate, and while strong growth is supportive, a prolonged higher rate environment creates a downside risk from this aspect.

The impact of higher energy prices:

- Whilst it is too early to understand the exact implications of higher energy prices, it is highly likely that we will be exposed to various unusual trend in income statements throughout the next 9 months. On page 27 of this report, we are providing an initial opinion as to in what sense and which companies will be impacted for now.

Model portfolio and stock recommendations

Excluding Yapi Kredi, Adding Akbank- Our reasons for the Akbank addition to the model portfolio is as follows: (1) The stock underperformed the banking index by 7.6% since the beginning of the year, in our view due to lower ROTE production compared to other private banks in H121. (2) at 0,37x P/BV (21E), the stock trades at an all time low multiple, and (3) the Bank should report much better results in H221 on lower risk indicators and margins and its ROTE should approach its peers.

- Despite we continue to like Yapı Kredi from a fundamental perspective, we are excluding the stock due to our intention not to raise the weight of banks in our portfolio. Additionally, a lock up limiting Unicredit, a minority shareholder (19.9%) to sell shares, which indicated to exit with its last exit in February 2020, is ending by mid-November. Hence, we prefer to be sidelined until there is clarity from this aspect.