Inflation in Turkey has continued to rise for the sixth consecutive month. The growth of consumer prices has reached 69.8% compared to the previous year, marking the fastest rate since late 2022 and an increase from 68.5% in March. Economists surveyed by Bloomberg had a median estimate slightly above 70%.

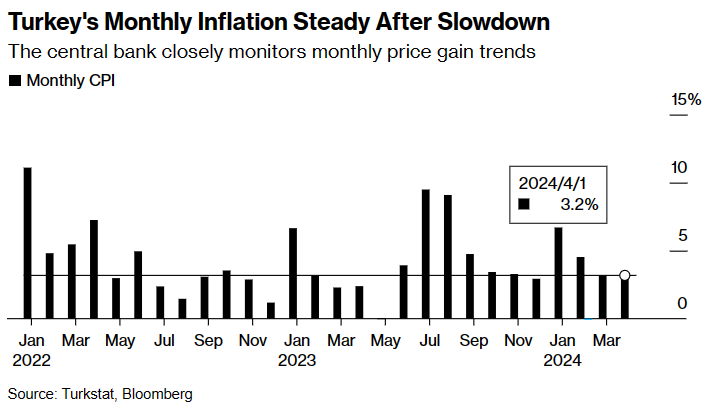

The central bank’s preferred measure, monthly price growth, remained stable at 3.18%. Turkish monetary officials have indicated that annual inflation is likely to reach its peak this month, before decelerating to 36% by year’s end.

The most recent statistics further substantiate that inflationary pressures persisted at high levels in April.

Inflation in the services sector increased to an annual rate of 97%, up from 96.5% in March, as per the official data. The inflation rate for core consumer goods, which is an index that excludes the influence of fluctuating items like food and energy, rose to 75.8% from 75.2%.

The seasonally adjusted monthly CPI inflation of 3.4% is still high, not yet in line with CBRT’s year-end inflation target of 36%.

On the other hand, B-Index and C-Index in core inflation increased by 3.24% and 3.56%, respectively, to 72.72% and 75.81% yoy. The previous month’s levels were 71.89% and 75.21%. This indicates that the underlying inflation trend continued to rise.

With the strong rise in energy prices, goods inflation rose from 58.17% to 59.67%. Inflation in unprocessed food prices in the goods group decreased from 84.14% to 77.85% due to seasonality. Processed food price inflation, on the other hand, rose from 597% to 60.19%. On the other hand, services price inflation remained at a very high level. It rose to 96.99 per cent this month from 96.48 per cent last month. Rental price inflation continued to rise, from 123.95% to 124.47%.

Under normal circumstances, CBRT should be expected to continue raising interest rates given the current course. However, in its latest MPC note, the Bank left the door open for rate hikes, but stated that it is in a wait-and-see period and that it will evaluate the lagged effects of monetary tightening on economic activity and pricing behaviour. It added that it will deepen the tightening with liquidity management.

CBRT is trying to reduce CPI inflation with gradual interest rate hikes without lowering 2024 growth below 3%, in a sense with a soft transition. Annual inflation, which will decline strongly with the base effect in the summer months, will fall to the range of 50-52%. However, at the end of the year, the expectation is still in the range of 44-48% and well above the target of 36%. CBRT’s 2025 inflation target of 14% seems unattainable. Although the latest economic data point to a slowdown in consumer loans, the level of domestic demand is still out of line with expectations. In this environment, if the CBRT is serious about its inflation targets, it should continue to raise interest rates in a way to risk a contraction in the economy. However, it is understood from its latest messages that it will not take such a step at the May MPC meeting for now.

In May last year, monthly inflation was manipulated by announcing 0.04% due to natural gas price manipulation. This year, even if the monthly expectation is around 3.3%, there will be a significant jump in annual inflation due to the low base effect and the annual inflation will exceed 75%. Instead of the two-month inflation of 19% in July-August last year, it will fall to around 51% with two-month inflation of 4-5% this year.